23andMe: the latest SPAC

Like our genes, 23andMe is a double-stranded opportunity

Earlier this month, 23andMe announced that it would be going public by merging with Richard Branson’s special purpose acquisition company, continuing the SPAC-tacular run of startups leveraging these blank check companies in place of traditional IPOs. Today we’re going to dive into the business and understand its history as well as the opportunities and challenges which lie ahead.

23andMe’s journey is a microcosm of tech in healthcare

Since it was established in 2006, 23andMe has in many ways embodied both the possibilities and perils of technology in healthcare. Its founding team spanned the two industries, with Anne Wojcicki, a healthcare investment analyst who is also the younger sister of Susan Wojcicki, the CEO of YouTube, and Linda Avey, a biologist involved in the world’s first genome-wide association studies (which we’ll talk more about later).

The company’s mission is to “help people access, understand, and benefit from the human genome”, and its main product offering to date has been direct-to-consumer genetic testing, where customers can order a testing kit online, provide a saliva sample, and receive insights about their DNA. Early on, 23andMe was a poster child for how technological progress could be used to revolutionize healthcare, and its saliva-based genotyping approach was named an Invention of the Year by Time in 2008.

The company’s press coverage was considerably less positive the next time it made a big splash in Nov 2013, when the FDA demanded it to stop selling its genome testing kits without authorization. The agency’s warning letter was colored with exasperation, raising serious questions about the company’s overarching strategy and approach with the FDA. At the time, Matthew Herper from Forbes wrote the following:

“Either 23andMe is deliberately trying to force a battle with the FDA, which I think would potentially win points for the movement the company represents but kill the company itself, or it is simply guilty of the single dumbest regulatory strategy I have seen in 13 years of covering the Food and Drug Administration.”

The genetic insights that 23andMe’s testing kits provide can largely be grouped into two categories — those that are ancestry-related and those that are health-related. The former includes mostly fun features that allow consumers to learn about their ancestors and locate distant relatives. But the latter is what got the company into trouble with the FDA, in which the testing results are used to identify risk factors for 250+ diseases and drug responses. Given the adverse health effects that could result from false-positive or negative outcomes, the FDA stated that compliance with regulatory requirements was needed “to ensure that the tests work”.

Since then, the company’s trajectory, at least from a regulatory standpoint, has improved substantially. On October 1, 2015, 23andMe received its first FDA approval, which allowed their genomic testing product to be marketed as a screening system for Bloom Syndrome. This was followed by a second approval in Apr 2017, which permitted the product to be used to determine genetic health risks for 10 different conditions, including Alzheimer’s and Parkinson’s. In total, the company has now obtained 6 approvals / clearances from the FDA.

23andMe’s core business is either struggling or thriving

On the surface, the timing of 23andMe’s SPAC is curious, considering the growth of the company’s genomic testing product has been anemic since 2019. Some view the slowdown as an indication that 23andMe has already saturated its market, while others have speculated that an increase in privacy concerns among consumers is tempering demand. The topic of privacy has certainly been front of mind for consumers the past few years, and we’ll come back to it later. But the notion that 23andMe has already saturated its market begs an all-important question — what exactly is the company’s market?

The simple answer is that their market consists of all consumers who are interested in sequencing and learning about their DNA. But public statements from the company’s leadership, as well as their SPAC investor presentation, imply a much larger vision in which their genomic testing product is simply a means to an end. Patrick Chung, a 23andMe board member, said the following in 2013:

“The long game here is not to make money selling kits, although the kits are essential to get the base level data. Once you have the data, the company does actually become the Google of personalized health care.”

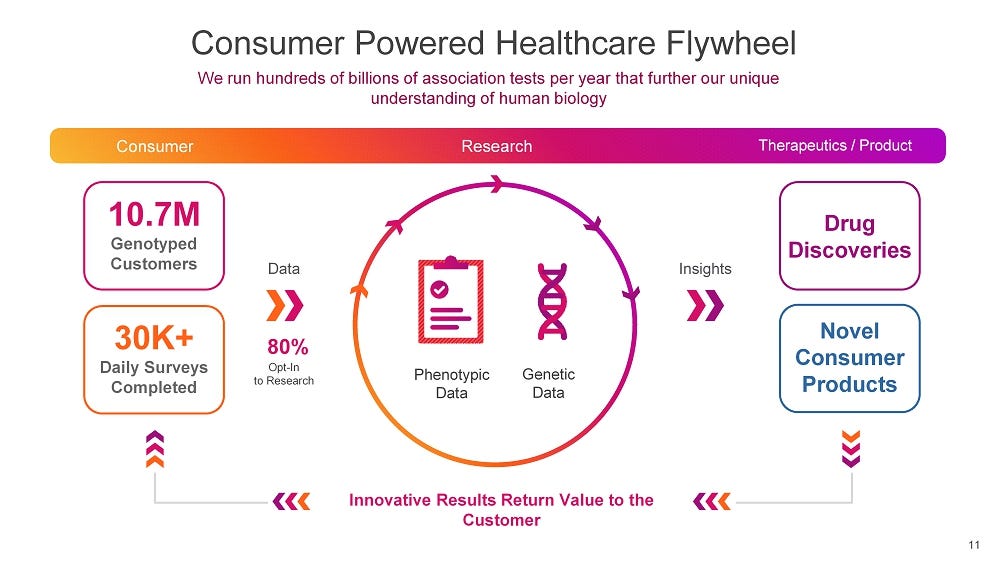

This broader vision is best illustrated through the flywheel below. On the frontend, the genome testing kits capture genetic data as well as phenotypic data from consumers who order them. Once the data has been captured and accumulated, 23andMe is able to run large-scale association studies to discover relationships between various genes and conditions. Then on the backend, the company is able to offer these unparalleled insights as a service to a whole array of healthcare stakeholders, including pharmaceutical companies and providers.

It’s extremely important to understand this point, because it completely redefines the company’s market opportunity and how to think about its future potential. In light of this, 23andMe is nowhere near saturating its market; in fact, the company has barely begun offering the service that may one day become its core business — monetizing troves of health data. Dismissing 23andMe at this point would be as foolish as dismissing Google in 2000 because the search market was too small.

With this broader vision in mind, the bottom line growth of 23andMe’s genomic testing business becomes less important. Instead, the question is whether the company has accumulated enough data to date to begin generating valuable insights and unlocking the second segment of its business. Answering this requires us to understand how exactly 23andMe takes genetic data and turns it into scientific discoveries.

The process revolves around what’s known as a genome-wide association study (GWAS), the type of study that Linda Avey, one of the company’s founders, pioneered almost 20 years ago. A GWAS takes genome-wide data from a large sample of individuals, along with each individual’s phenotype for a given trait or condition, and looks for significant associations between certain genetic variants and conditions. The objective is to uncover linkages which may signal a functional relationship between a given variant and the disease, and lead to a better understanding of the underlying biology. An important advantage of GWAS studies is that it is a non-candidate-driven approach, in which associations can be identified without selecting genes of interest beforehand.

One major drawback of GWAS studies is the number of patients needed. The sample size for a given GWAS depends on several factors, including the frequency of various genetic variants and their phenotypic effect sizes, but no matter what, a boatload of data is required. This is why 23andMe’s strategy of starting with consumer genetic testing makes sense, because it allows them to generate revenue from a near-term product while building up a database of genetic profiles that enables their long-term vision.

The company’s SPAC presentation suggests that they reached a critical mass last year, surpassing more than 10m genotyped customers. There’s a footnote in the deck which sharpens this point — 23andMe is now able to conduct GWAS studies with more than 10,000 cases even for conditions with only a 0.1% prevalence. For more common conditions, their database will almost certainly contain millions of cases that can be analyzed.

Another drawback of GWAS studies is their cost, which can total hundreds of millions of dollars for a single investigation, without any guarantee of success. This might be the most compelling piece of 23andMe’s strategy. Unlike traditional GWAS studies, where researchers often have to recruit thousands of participants from scratch to answer each scientific question, 23andMe is able to constantly run tests on the dataset it has accumulated to uncover new findings. In other words, they have created a platform for conducting incredibly powerful GWAS studies with almost zero marginal cost. All of this is further supported by a flywheel effect — simple math dictates that as the number of individuals they have genotyped increases, the number of GWAS hits (aka significant associations) they find will increase as well.

So how is the company looking to capitalize on what it has built? At the moment, the company’s strategy in its second vertical seems to revolve around its exclusive partnership with GlaxoSmithKline (GSK) which was announced in 2018. As part of the deal, GSK invested $300m into 23andMe and the two agreed to co-develop a pipeline of therapeutics, using 23andMe’s data and research platform to make the process faster and more efficient. The two companies launched their first joint clinical trial in humans July of last year, and have 5 more assets in the preclinical stage. While it will be years before 23andMe starts to generate revenue from this collaboration, it is also only a hint of what the company can do with the remarkable dataset it has brought together.

23andMe should learn from data-centric tech companies

The idea of building a company almost entirely around data is rather new in healthcare, but it’s been wildly successful in the tech industry, and 23andMe should learn from the companies that have done it already. One specific area to keep an eye on is pricing. Companies like Google and Facebook, which have data at the heart of their business models, have demonstrated the importance of lowering the barrier to entry as much as possible for consumers. In many cases, this means making the product itself free, and then subsidizing the cost of developing the product by monetizing the data that’s captured.

Considering the outsized benefits of having a larger genetic database, 23andMe should try and make their genome testing kits as cheap and accessible as possible. It would be entirely sensible for the company to run their consumer testing business at a substantial loss, to prioritize growth and scale. This may be challenging in the near-term, before the company starts to actually generate revenue from their health insights business, but it would pay off in the long run.

23andMe should also be very closely following the broader debate around consumer data in tech. The company should be proactive in establishing a privacy-first brand and culture, and defining guidelines for how customer health data will and won’t be used. 23andMe may end up having an easier time than a company like Facebook on this front, because the former plans to leverage de-identified, population-level data, whereas the latter relies on hyper-targeted personalization. That said, privacy concerns will remain the single biggest risk for 23andMe in achieving its vision. It’s one thing for consumers to find out that their favorite movies or TV shows have been leaked, and another to discover that their genetic predisposition for cancer has been exposed or misused.

In a time when digital health companies are thriving across the board, 23andMe is a rare example of a company truly leveraging the fundamental advantages of technology to rethink healthcare. Over the past 15 years, the company has deftly built up one of the most unique and prized datasets in the world, and it now has the opportunity to execute on an enormous and admirable vision. For this, it is still early days, and the company will have to learn from both the successes and mistakes of tech companies today to become the foremost health tech company of tomorrow.